December CPI Report: Inflation Slowdown Defies Expectations

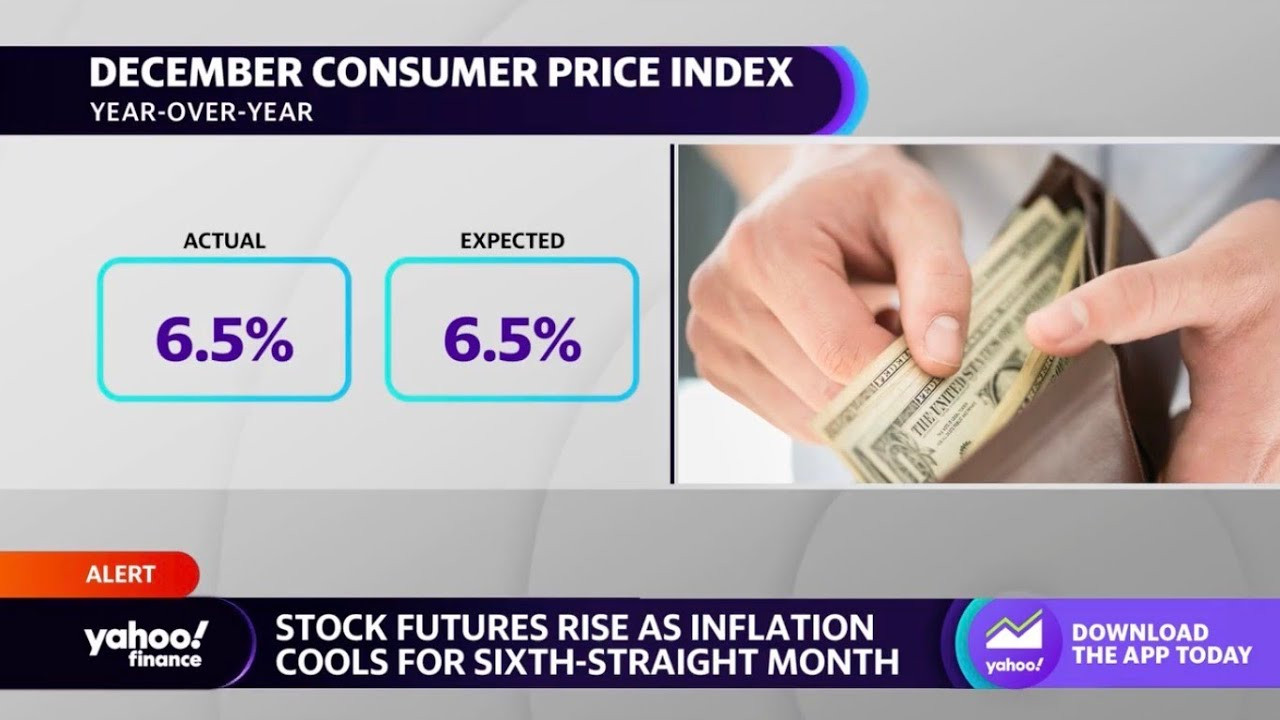

Prices that consumers pay for a variety of goods and services rose again in December, but closed out 2024 with some mildly better news on inflation, particularly on housing. The consumer price index increased a seasonally adjusted 0.4% on the month, putting the 12-month inflation rate at 2.9%, the Bureau of Labor Statistics reported Wednesday. Economists surveyed by Dow Jones had been looking for respective readings of 0.3% and 2.9%.

Core CPI and Market Reactions

However, excluding food and energy, the core CPI annual rate was 3.2%, a notch down from the month before and slightly better than the 3.3% forecast. The core measure rose 0.2% on a monthly basis, also 0.1 percentage point less than expected. Much of the move higher in the CPI came from a 2.6% gain in energy prices for the month, pushed higher by a 4.4% surge in gasoline. That was responsible for about 40% of the index's gain, according to the BLS. Food prices also rose, up 0.3% for the month. On an annual basis, food climbed 2.5% in 2024 while energy nudged down by 0.5%. Shelter prices, which comprise about one-third of the CPI weighting, rose by 0.3% but were up 4.6% from a year ago, the smallest one-year gain since January 2022. Services prices excluding rents rose 4% from a year ago, the slowest since February 2024.

Stock market futures surged following the release while Treasury yields tumbled. Though the numbers compared favorably to forecasts, they still show that the Federal Reserve has work to do to reach its 2% inflation target. Headline inflation moved down from its 3.3% rate in 2023, while core was 3.9% a year ago.

Fed's Response and Economic Outlook

The inflation readings this week – the BLS released its producer price index Tuesday – are expected to keep the Fed on hold when it convenes its policy meeting later this month. While the market cheered the CPI release, the news was less positive for workers: Inflation-adjusted hourly earnings for the month fell by 0.2%, putting the year-over-year gain at just 1%, the BLS said in a separate release. Details in the inflation report otherwise were mixed. Used car and truck prices jumped 1.2% while new vehicle prices also moved higher by 0.5%. Transportation services surged 0.5% and were up 7.3% year over year, while egg prices jumped 3.2%, taking the annual gain to 36.8%. Auto insurance rose 0.4% and was up 11.3% annually.

"The inflation rate is currently grappling with a 'last mile' problem, where progress in reducing price pressures has slowed," said Sung Won Sohn, a professor at Loyola Marymount University and chief economist at SS Economics. "Key drivers of inflation, including gas, food, vehicles, and shelter, remain persistent challenges. However, there are signs of hope that long-term inflationary pressures may continue to ease, aided by moderating trends in critical sectors such as shelter and labor costs."

The report comes with markets skittish over the state of inflation and the Fed's potential response. Tariffs and mass deportations that President-elect Donald Trump has promised have increased concerns over inflation. Job growth in December was much stronger than economists had expected, with the gain of 256,000 further raising concerns that the Fed could stay on hold for an extended period and even contemplate interest rate increases should inflation prove stickier than expected. The December CPI report, coupled with a relatively soft reading Tuesday on wholesale prices, shows that while inflation is not cooling dramatically, it also isn't indicating signs of reaccelerating. A separate report Wednesday from the New York Fed showed manufacturing activity softening but prices paid and received rising substantially. Futures pricing continued to imply a near certainty that the Fed would stay on hold at its Jan. 28-29 meeting but titled more favorably toward two rate cuts through the year, assuming quarter percentage point increments, according to CME Group figures. Markets expect the next cut likely will happen in May or June. The Fed uses the Commerce Department's personal consumption expenditures price index as its primary forecasting measure for inflation. However, the CPI and PPI measures figure into that calculation. The two readings likely mean that the core PCE will rise just 0.2% in December, keeping the annual rate at 2.8%, according to Samuel Tombs, chief U.S. economist at Pantheon Macroeconomics.

The Inflation Puzzle: A Deeper Dive

Recently, progress on inflation appeared to be stuck or, at worst, reversing: A closely watched gauge of underlying price hikes — an index that excludes highly volatile categories — hadn’t budged for months. On Wednesday, it got unstuck. The closely watched core measurement of the Consumer Price Index slowed for the first time in months, according to Bureau of Labor Statistics data released Wednesday. That reading, coupled with some better-than-expected wholesale inflation data received on Tuesday, spurred optimism in the markets. US stock futures spiked Wednesday morning, as the CPI report boosted traders’ hopes that the Federal Reserve will continue its rate-cutting campaign this year. Futures on the Dow rose by more than 600 points. Futures on the S&P moved up by 1.5% and Nasdaq futures were higher by 1.8%. Overall, the Consumer Price Index did increase more than anticipated, rising 0.4% from November and jumping 0.2 percentage points to an annual rate of 2.9%. However, the increase was largely driven by gas and food prices. Energy prices, particularly gas and fuel costs, accounted for 40% of the overall monthly increase. Food prices also remained elevated as key staples such as meat and eggs continued to face pressures from weather and disease, respectively. However, in the context of inflation measures, energy and food are two of the most volatile categories and can exhibit wild swings because of factors considered one-time in nature. Excluding energy and food, the closely watched core CPI gauge slowed for the first time in months, rising just 0.2% from November and easing to 3.2% after staying stuck at 3.3% since September 2024. Wednesday’s report marked the final CPI reading for 2024 and the last before President Joe Biden hands the keys over to President-elect Donald Trump. While the causes of this recent bout of inflation were multifaceted and largely related to the Covid-19 pandemic and its fallout, the sharp rise in prices hit Americans hard and proved to be a critical factor at the ballot box. Economists were expecting inflation to pick up 0.3% from November and notch a 2.8% annual increase, primarily due to expectations around higher energy and food prices. The CPI measures price changes across commonly purchased goods and services. The slight 0.2% rise in production from October is insufficient to indicate a reversal of the two-year downward trend. Overall, the outlook for industry remains quite weak at the start of the year.

Unpacking the Implications: What Lies Ahead?

Inflation in the US, as measured by the change in the Consumer Price Index (CPI), rose 2.9% on a yearly basis in December from 2.7% in November. This reading came in line with market expectations. On a monthly basis, the CPI rose 0.4%, following the 0.3% increase recorded in the previous month. The core CPI, which excludes volatile food and energy prices, rose 3.2% on a yearly basis—below November’s gain and analysts’ estimates for a 3.3% increase. The monthly core CPI rose 0.2% in the last month of 2024. The Greenback rapidly breaks below the 109.00 support when tracked by the US Dollar Index (DXY) in the wake of the release of US CPI data, hitting at the same time new multi-day lows. The incoming Trump administration is expected to take a stricter stance on immigration, adopt a more relaxed fiscal policy, and reintroduce tariffs on imports from China and Europe. These factors, combined with a resilient labour market, are likely to put upward pressure on inflation and have already started to reshape investor expectations. Markets now anticipate that the Federal Reserve will cut interest rates by just 25 basis points this year, keeping the outlook for the US Dollar stable for now. However, with the US labour market cooling at a slow pace and inflation remaining stubbornly high, the December inflation report is unlikely to prompt any major shifts in the Fed’s monetary policy. Currently, CME Group’s FedWatch Tool indicates a 97% probability that the Fed will leave rates unchanged at its January 29 meeting. Although it may seem counter-intuitive, high inflation in a country pushes up the value of its currency and vice versa for lower inflation. This is because the central bank will normally raise interest rates to combat the higher inflation, which attract more global capital inflows from investors looking for a lucrative place to park their money. The December CPI report signals "little relief to most consumers." Food prices, which had been tame in the first half of 2024, continued their acceleration, increasing 0.3% in December. The increases in prices of items closely watched by consumers could continue to be a drag on consumer confidence, which has already shown weakness on inflation concerns. The Fed's next move remains uncertain, but the December CPI data offers a glimmer of hope that the inflation battle is not yet lost. The economic future however remains complex, influenced by numerous factors. The market's reaction to the report suggests that some investors see the current trend as positive, while others may remain apprehensive due to uncertainties surrounding the incoming administration's economic policies.